PERSONAL FINANCE

How to Stop Living Paycheck to Paycheck: A Real System

You're Not Bad With Money

Let's get this out of the way first: living paycheck to paycheck is not a character flaw.

61% of Americans report living paycheck to paycheck as of 2025. That number includes people earning six figures. It's not an income problem or a discipline problem — it's a systems problem.

When you don't have a system, money flows out as fast as it flows in. Not because you're reckless, but because invisible spending adds up faster than you expect, and nothing is stopping it.

The fix isn't cutting your Starbucks. The fix is building a system.

Why Most People Can't Break the Cycle

The paycheck-to-paycheck trap has three root causes:

1. No buffer between income and expenses

Every dollar of income is already spoken for. One unexpected expense — a car repair, a medical bill, a forgotten annual subscription — immediately creates a deficit.

2. No visibility into upcoming expenses

You can't prepare for what you can't see. Most people have no idea that $800 in bills is hitting in the next 10 days.

3. Savings treated as optional

When savings happen only if there's "something left over," they never happen. There's never something left over.

The System That Actually Works

Phase 1: Create a $1,000 emergency buffer (before anything else)

This is your firewall. Before you pay extra on debt, before you invest, before you do anything else — get $1,000 in a dedicated savings account that you do not touch.

This single step breaks the cycle for most people because it absorbs the unexpected expenses that previously sent everything off the rails.

To get there faster: sell something, take an extra shift, pause one subscription for 60 days. Do whatever it takes to build this buffer in the next 30 days.

Phase 2: Map every bill to its due date

List every fixed expense and when it's due. Not generally "monthly" — the exact date. Then add up all expenses due in the next 14 days. That number is your baseline — your account should never drop below it.

Phase 3: Set up automatic savings on payday

The moment your paycheck hits, $X goes to savings automatically. Not at the end of the month. Not when you remember. The moment it arrives.

Start with whatever is realistic — even $25 per paycheck. The habit matters more than the amount right now.

Phase 4: Give every paycheck a job before you spend it

When your paycheck arrives, allocate it immediately:

What's left is what you can actually spend. This is zero-based budgeting at its most practical.

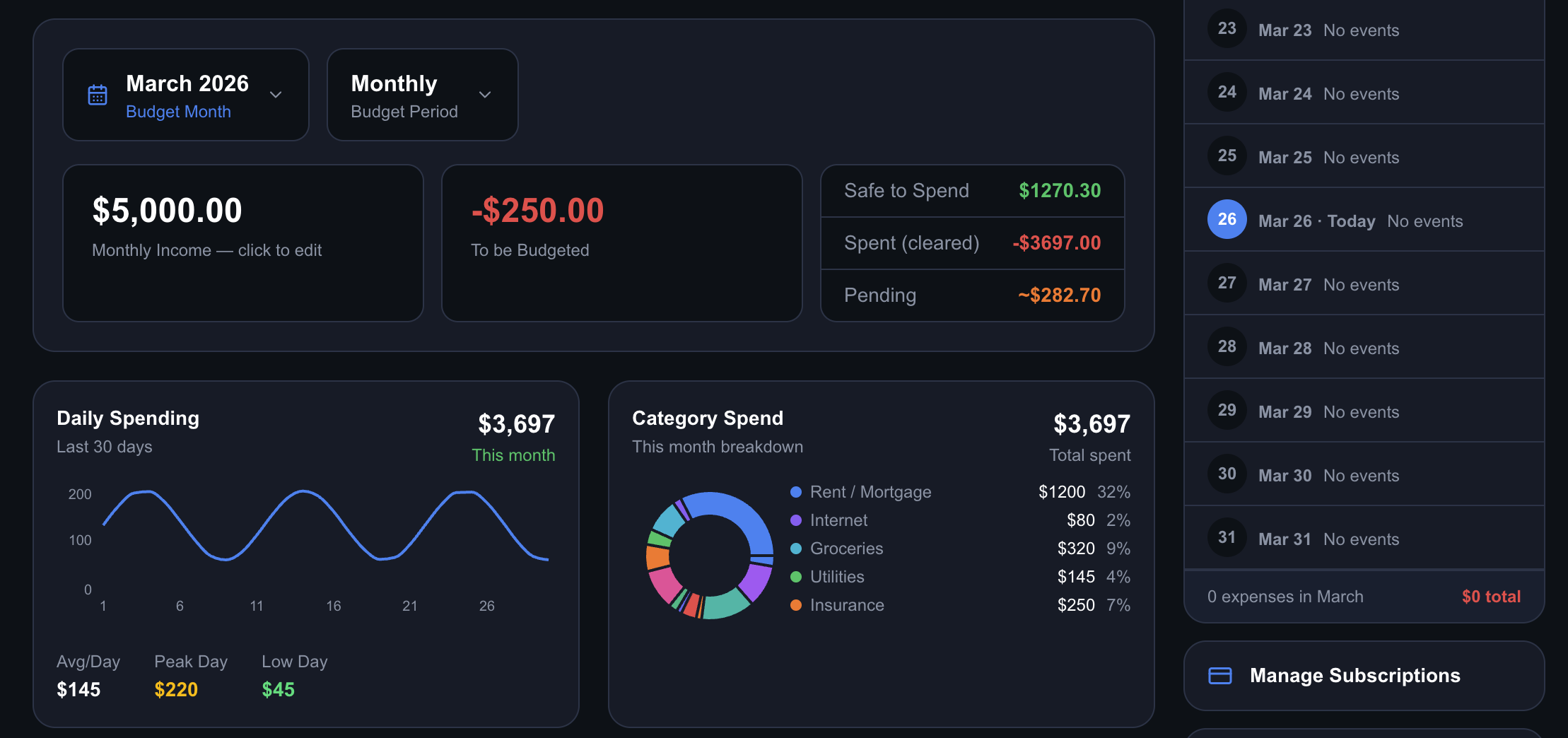

Blueprint Makes Phase 2 and 4 Automatic

The hardest part of this system is phases 2 and 4 — knowing exactly what's coming and allocating your paycheck before you spend it.

Blueprint connects to your bank (via Plaid) and your calendar, then builds a live picture of exactly what's hitting your account and when.

You can see:

When you open Blueprint after a paycheck hits, it shows you immediately: here's what needs to be covered in the next two weeks, here's what you have, here's what's left to spend. No math required.

What Six Months Looks Like

Month 1: $1,000 emergency buffer funded. Bills mapped. Spending no longer invisible.

Month 2: First month without an overdraft or "surprise" expense derailing you. Buffer absorbed a $200 car repair.

Month 3: First automatic savings transfer stays put. $300 in savings.

Month 4: Savings habit locked in. Starting to see the budget calendar working — you're planning around your money instead of reacting to it.

Month 6: You realize you haven't thought "I can't wait for payday" in weeks.

That's the cycle breaking. Not dramatically — gradually, then completely.

Start your system with Blueprint. Free for 30 days.

TRY BLUEPRINT FREE

Your budget, your calendar, your goals — unified.

30-day free trial. Connect your bank and calendar in under 10 minutes.

Start Free Trial